Greg Montgomery, CFP/CPA

Chief Financial Officer, Board Member and Former Big 4 CPA

Corporate Deal Making

Corporate deal making has a new look—smaller, busier, and focused on growth. Not so long ago, M&A experts sequenced, at most, 3 or 4 major deals a year, typically with an eye on the benefits of industry consolidation and cost cutting. Today I regularly come across executives hoping to close 10 to 20 smaller deals in the same amount of time, often simultaneously. Their objective: combining a number of complementary deals into a single strategic platform to pursue growth—for example, by acquiring a string of smaller businesses and melding them into a unit whose growth potential exceeds the sum of its parts.

Naturally, when executives try to juggle more and different kinds of deals simultaneously, productivity may suffer as managers struggle to get the underlying process right.1 Most companies, I have found, are not prepared for the intense work of completing so many deals—and fumbling with the process can jeopardize the very growth companies seek. In fact, most of them lack focus, make unclear decisions, and identify potential acquisition targets in a purely reactive way. Completing deals at the expected pace just can’t happen without an efficient end-to-end process.

Even companies with established deal-making capabilities may have to adjust them to play in this new game. Our research shows that successful practitioners follow a number of principles that can make the adjustment easier and more rewarding. They include linking every deal explicitly to the strategy it supports and forging a process that companies can readily adapt to the fundamentally different requirements of different types of deals.

Eyes on the Strategic Prize

One of the most often overlooked, though seemingly obvious, elements of an effective M&A program is ensuring that every deal supports the corporate strategy. Many companies, I have found, believe that they are following an M&A strategy even if their deals are only generally related to their strategic direction and the connections are neither specific nor quantifiable.

Instead, those who advocate a deal should explicitly show, through a few targeted M&A themes, how it advances the growth strategy. A specific deal should, for example, be linked to strategic goals, such as market share and the company’s ability to build a leading position. Bolder, clearer goals encourage companies to be truly proactive in sourcing deals and help to establish the scale, urgency, and valuation approach for growth platforms that require a number of them. Executives should also ask themselves if they have enough people developing and evaluating the deal pipeline, which might include small companies to be assembled into a single business, carve-outs, and more obvious targets, such as large public companies actively shopping for buyers.

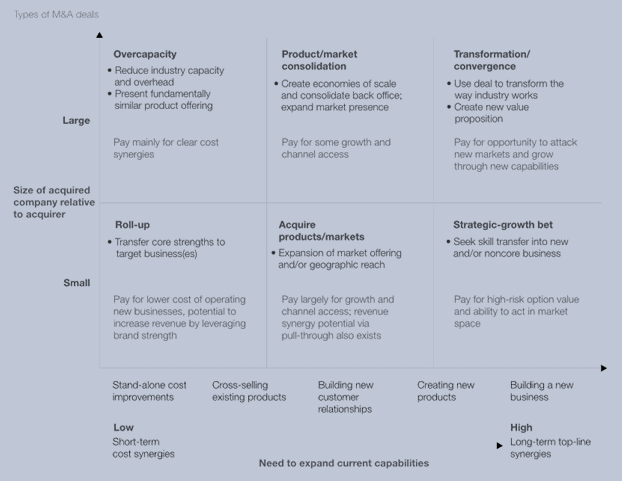

Furthermore, many deals underperform because executives take a one-size-fits-all approach to them—for example, by using the same process to integrate acquisitions for back-office cost synergies and acquisitions for sales force synergies. Certain deals, particularly those focused on raising revenues or building new capabilities, require fundamentally different approaches to sourcing, valuation, due diligence, and integration. It is therefore critical for managers not only to understand what types of deals they seek for shorter-term cost synergies or longer-term top-line synergies (Exhibit 1), but also to assess candidly which types of deals they really know how to execute and whether a particular transaction goes against a company’s traditional norms or experience.

Exhibit 1 – Managers must understand not only which types of deals they desire, but also which types they know how to execute.

Companies with successful M&A programs typically adapt their approach to the type of deal at hand. For example, over the past six years, IBM has acquired 50 software companies, nearly 20 percent of them market leaders in their segments. It executes many different types of deals to drive its software strategy, targeting companies in high-value, high-growth segments that would extend its current portfolio into new or related markets. IBM also looks for technology acquisitions that would accelerate the development of the capabilities it needs. Deal sponsors use a comprehensive software-segment strategy review and gap analysis to determine when M&A (rather than in-house development) is called for, to identify targets, and to determine which acquisitions should be executed.

IBM has developed the methods, skills, and resources needed to execute its growth strategy through M&A and can reshape them to suit different types of deals. A substantial investment of money, people, and time has been necessary. IBM’s software group alone was concurrently integrating 18 acquisitions; more than 100 full-time experts in a variety of functions and geographies Ire involved, in addition to specialized teams mobilized for each deal. IBM’s ability to tailor its approach has been critical in driving the performance of these businesses. Collectively, IBM’s 39 acquisitions below $500 million doubled their direct revenue within two years.

Organization & Process

When companies increase the number and pace of their acquisitions, the biggest practical challenge most of them face is getting not only the right people but also the right number of people involved in M&A. If they don’t, they may buy the wrong assets, underinvest in appropriate ones, or manage their deals and integration efforts poorly. Organizations must invest to build their skills and capabilities before launching an aggressive M&A agenda.

Support from Senior Management

In many companies, senior managers are often too impressed by what appears to be a low price for a deal or the allure of a new product. They then fail to look beyond the financials or to provide support for integration. At companies that handle M&A more productively, the CEO and senior managers explicitly identify it as a pillar of the overall corporate strategy. At GE, for example, the CEO requires all business units to submit a review of each deal. In addition to the financial justification, the review must articulate a rationale that fits the story line of the entire organization and spell out the requirements for integration. A senior vice president then coaches the business unit through each phase of a stage gate process. Because the strict process preceding the close of the deal outlines what the company must do to integrate the acquisition, senior management’s involvement with it after the close is defined clearly.

The most common challenge executives face in a deal is remaining involved with it and accountable for its success from inception through integration. They tend to focus on sourcing deals and ensuring that the terms are acceptable, quickly moving on to other things once the letter of intent is signed and leaving the integration work to anyone who happens to have the time. To improve the process and the outcome, executives must give more thought to the appointment of key operational players, such as the deal owner and the integration manager.

The Deal Owner

Deal owners are typically high-performing managers or executives accountable for specific acquisitions, beginning with the identification of a target and running through its eventual integration. The most successful acquirers appoint the deal owner very early in the process, often as a prerequisite for granting approval to negotiate with a target. This assignment, which may be full or part time, could go to someone from the business-development team or even a line organization, depending on the type of deal. For a large one regarded as a possible platform for a new business unit or geography, the right deal owner might be a vice president who can continue to lead the business once the acquisition is complete. For a smaller deal focused on acquiring a specific technology, the right person might be a director in the R&D function or someone from the business-development organization.

The Integration Manager

Often, the most underappreciated and poorly resourced role is that of the integration manager—in effect, the deal owner’s chief of staff. Typically, integration managers are not sufficiently involved early in the deal process. Moreover, many of them are chosen for their skills as process managers, not as general managers who can make decisions, work with people throughout the organization, and manage complicated situations independently.

Integration managers, our experience shows, ought to become involved as soon as the target has been identified but before the evaluation or negotiations begin. They should drive the end-to-end merger-management process to assure that the strategic rationale of a deal informs the due diligence as well as the planning and implementation of the integration effort. During IBM’s acquisition of Micromuse, for example, a vice president–level executive was chosen to take responsibility for integration. This executive was brought into the process Ill before due diligence and remains involved almost two years after the deal closed. IBM managers attribute its strong performance to the focused leadership of the integration executive.

Sizing a Professional Merger Management Function

Companies that conclude deals only occasionally may be able to tap functional and business experts to conduct due diligence and then build integration teams around specific deals. But a more ambitious M&A program entails a volume of work—to source and screen candidates, conduct preliminary and final due diligence, close deals, and drive integration—that demands capabilities and processes on the scale of any other corporate function. Indeed, our experience with several active acquirers has taught us that the number of resources required can be quite large (Exhibit 2). To do 10 deals a year, a company must identify roughly 100 candidates, conduct due diligence on around 40, and ultimately integrate the final 10. This kind of effort requires the capacity to sift through many deals while simultaneously managing three or four data rooms and several parallel integration efforts. Without a sufficient (and effective) investment in resources, individual deals are doomed to fail.

Exhibit 2 – Making a large number of deals requires a real investment in resources.

A Rigorous Stage Gate Process

A company that transacts large numbers of deals must take a clearly defined stage gate approach to making and managing decisions. Many organizations have poorly defined processes or are plagued with choke points, and either fault can make good targets walk away or turn to competitive bids. Even closed deals can get off to a bad start if a target’s management team assumes that a sloppy M&A process shows what life would be like under the acquirer.

An effective stage gate system involves three separate phases of review and evaluation. At the strategy approval stage, the business-development team (which includes one or two members from both the business unit and corporate development) evaluates targets outside-in to assess whether they could help the company grow, how much they are worth, and their attractiveness as compared with other targets. Even at this point, the team should discuss key due diligence objectives and integration issues. A subset of the team then drives the process and assigns key roles, including that of the deal owner. The crucial decision at this point is whether a target is compatible with the corporate strategy, has strong support from the acquiring company, and can be integrated into it.

At the approval-to-negotiate stage, the team decides on a price range that will allow the company to maintain pricing discipline. The results of preliminary due diligence (including the limited exchange of data and early management discussions with the target) are critical here, as are integration issues that have been revealed, at least to some extent, by the corporate functions. A vision for incorporating the target into the acquirer’s business plan, a clear operating program, and an understanding of the acquisition’s key synergies are important as Ill, no matter what the size or type of deal. At the end of this stage, the team should have produced a nonbinding term sheet or letter of intent and a roadmap for negotiations, confirmatory due diligence, and process to close.

The board of directors must endorse the definitive agreement in the deal approval stage. It should resemble the approval-to-negotiate stage if the process has been executed Ill; the focus ought to be on answering key questions rather than raising new strategic issues, debating valuations, or looking ahead to integration and discussing how to estimate the deal’s execution risk.

Each stage should be tailored to the type of deal at hand. Small R&D deals don’t have to pass through a detailed board approval process but may instead be authorized at the business or product unit level. Large deals that require significant regulatory scrutiny must certainly meet detailed approval criteria before moving forward. Determining in advance what types of deals a company intends to pursue and how to manage them will allow it to articulate the trade-offs and greatly increase its ability to handle a larger number of deals with less time and effort.

As companies adapt to a faster-paced, more complicated era of M&A deal making, they must fortify themselves with a menu of process and organizational skills to accommodate the variety of deals available to them.

Business Development Excellence

- Provide price competitiveness and service excellence.

- Create attractive capital investment opportunities from leveraging contacts, selectively participating in data rooms, private equity exits, non-core MLP assets, private sellers not widely shopped, legislation forced and global shifts driving new markets.

- Seek long-term EBITDA driven by strong demand in direct relation to population and demographic growth.

- Seek targeted market and geographic acquisition, expansion and operation strategy in diversified markets lacking necessary infrastructure that is strategic to the economy.

- Look for asset bases that facilitate financial leverage and provide for competitive advantage.

- Bring opportunities to market at reasonable multiples and flexible and creative deal terms that provide the most favorable economic incentive payout to management.

- Company needs long-lived, fee based assets supported by long-term contracts with credit worthy customers.

- Look for acquisitions with a strong organic growth profile, high density of customers and logistically advantaged.

- Development of differentiated investment theses, enhancing deal flow by profiling industries, screening companies and devising plans to approach targets. Developing knowledge and sourcing advantages to mitigate and reduce risk.

- Experience that spans all relevant aspects of industry with vital network of deep relationships brought to bear in value-adding ways for company.

- Passionate about engaging with partners and frequently source deals for companies. Develop differentiated investment theses, enhance deal flow by profiling industries, screening companies and devising plans to approach targets.

- Support pursuit of rapid returns by developing a strategic blueprint for the acquired company, leading workshops that align management with strategic priorities and directing focused initiatives.